The right card depends on how you spend. Here’s how the top options in Singapore stack up.

The best corporate card for a Singapore SME isn’t necessarily the one with the highest cashback rate or biggest welcome bonus. It’s the one that matches how your business actually spends.

Whether you’re paying overseas suppliers, covering SaaS subscriptions, entertaining clients locally, or booking frequent business travel, choosing the wrong card can mean losing money to FX markups, annual fees, and missed rewards. Choose the right one, and it can deliver meaningful savings month after month.

In this guide, we compare some of the most popular corporate cards and business spend solutions in Singapore for 2026, including offerings from DBS, OCBC, UOB, and Maybank, miles-focused options like the American Express Singapore Airlines Business Credit Card, and the major multi-currency fintech accounts (Aspire, WorldFirst, Wise, Revolut, Airwallex, and YouBiz).

To make the comparison more useful, we’ve grouped each option by the type of business spender it’s best suited for.

Best Corporate Card in Singapore for SMEs (2026)

| Best for | Card | Headline reward | Annual fee | Network |

|---|---|---|---|---|

| Overseas & FX-heavy spend | YouBiz | Real 0% FX + unlimited 1% cashback | S$0 | Mastercard |

| Local F&B + travel cashback | DBS World Business Card | 2% FX rebate, 1% local F&B/travel | S$414.20 (1yr waiver) | Mastercard |

| Eco-friendly business spend | OCBC Business Credit Card | Up to 3% green merchants, 1% FX | S$196.20 | Visa/Mastercard |

| Lounge access + corporate cover | UOB Empire World Business (by invitation) | Up to 1.5% rebate + 1,300+ lounges | S$387.10 (1yr waiver) | Mastercard |

| Travel miles on SQ | Amex Singapore Airlines Business | Up to 8 miles per S$1 on SQ/Scoot | S$400 | Amex |

| SaaS & ad spend cashback | Aspire Corporate Card | 1% on online marketing + SaaS | S$0 card fees | Visa |

| Cross-border e-commerce | WorldFirst World Card (debit) | Up to 1.2% uncapped + 0% FX | S$0 card fees | Mastercard |

| Holding & paying in many currencies | Wise Business (debit) | 40+ currencies, mid-market + from 0.26% | S$0/mo (S$99 setup) | Visa/Mastercard |

| All-in-one account + FX allowance | Revolut Business (debit) | Interbank FX up to plan cap, then 0.6% | From S$0/mo | Visa/Mastercard |

| Global e-commerce + 1% cashback | Airwallex (debit) | 1% cashback + 0% FX from balance | S$0/mo (Explore) | Visa |

For many SMEs, the biggest cost of a corporate card isn’t the annual fee. It’s the FX markup charged on overseas transactions. Depending on your spending profile, those fees can outweigh the cashback earned, which is why low-FX and multi-currency business spend solutions have become increasingly popular.

Table of Contents

- What Makes a Corporate Card “Best” for an SME?

- How to Choose the Right Corporate Card for Your Business

- Best Corporate Cards in Singapore, Compared

- Multi-Currency Business Accounts, Side by Side

- The Best Corporate Card Depends on Your Priorities

- Don’t Overlook FX Fees: They Quietly Eat Your Rewards

- Final Takeaway

- FAQ

What Makes a Corporate Card “Best” for an SME?

Instead of focusing on headline cashback rates, SME value usually comes down to three factors.

1. Where you actually spend

Most cards reward dining, entertainment, and travel at higher rates, but offer minimal returns on everyday business spend like SaaS, ads, payments, suppliers, and cloud services. If your spending is mostly operational, category-based rewards matter less.

2. FX fees and hidden costs

Foreign exchange markups of 2.5%–3.5% are one of the biggest silent costs for SMEs. For a business spending S$50,000 overseas annually, that’s S$1,250–S$1,750 lost in fees alone, often more than the cashback earned.

3. Eligibility and ease of approval

Bank corporate cards may require operating history, financial statements, or director guarantees. Newer SMEs may find approval harder, regardless of how strong the rewards look on paper.

⚖️ In short: the best card is the one that matches your spending, reduces unnecessary fees, and is realistically accessible to your business.

How to Choose the Right Corporate Card for Your Business

With so many options available, the quickest way to narrow your shortlist is to evaluate cards through three lenses: your business stage, spending pattern, and eligibility.

By Business Stage

- Startups and newly incorporated businesses (0–2 years): Fintech options like YouBiz, Aspire, Wise, Revolut, Airwallex, and WorldFirst typically offer faster onboarding and simpler requirements compared to traditional bank cards.

- Established SMEs (3+ years): More options open up, including full bank corporate card suites. At this stage, spending behaviour matters more than eligibility.

By Spend Pattern

- FX-heavy businesses: If you pay overseas suppliers, SaaS tools, or run international ads, FX fees matter more than cashback. Prioritise cards with low or zero FX costs.

- Local dining, entertainment, and travel: Businesses that spend heavily on client meetings, corporate entertainment, and domestic travel may benefit from traditional bank cards that offer enhanced rewards in these categories.

- General day-to-day spending: If your expenses are spread across multiple categories, a flat cashback structure can be more valuable than category-specific rewards. Cards that offer uncapped cashback without minimum spending requirements provide predictable returns without the need to track bonus categories.

- Frequent Singapore Airlines travellers: Businesses that regularly book flights with Singapore Airlines or Scoot may find a miles-focused card more rewarding, especially if accumulating KrisFlyer miles is a priority.

By Eligibility Requirements

- Traditional bank corporate cards: Eligibility criteria vary by bank, but may include factors such as business age, annual revenue, financial statements, and director guarantees. Requirements are typically assessed on a case-by-case basis.

- Fintech business spend cards: Many fintech providers offer a streamlined onboarding process, often requiring only a registered Singapore business and identity verification from a director or authorised representative. This can make them more accessible for younger and fast-growing businesses.

The best corporate card isn’t defined by its rewards alone. It’s defined by how well it aligns with your spending patterns, cost structure, and ability to qualify.

Best Corporate Cards in Singapore, Compared

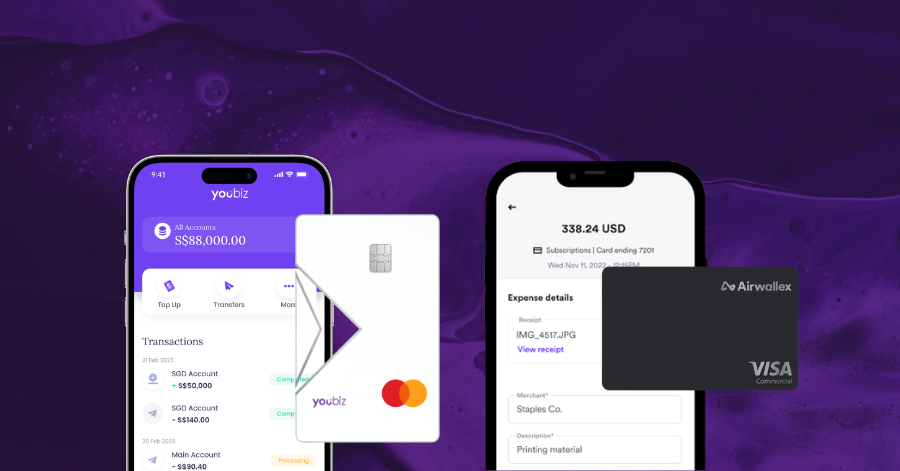

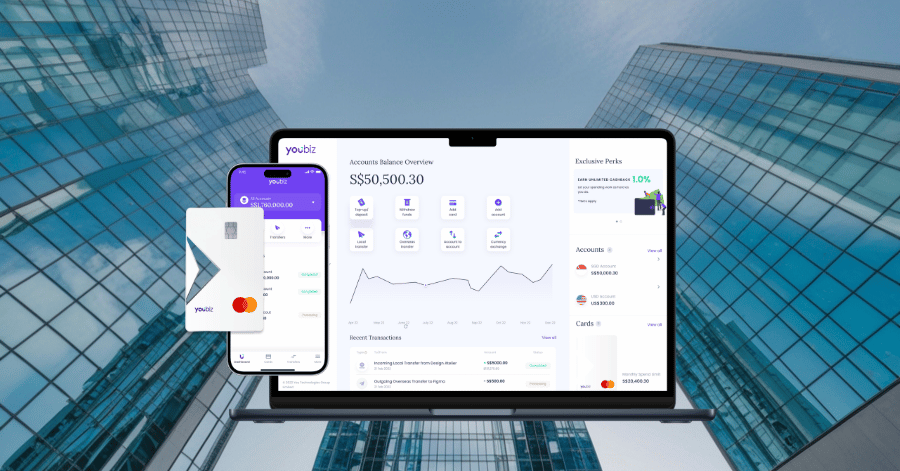

YouBiz: Best for Cross-Border SME Spend

The multi-currency business spend account from YouTrip and Mastercard. Sits closer to Wise Business or Airwallex than to a bank corporate card, but issued in Singapore and licensed by MAS.

- Rewards: Unlimited 1% on every eligible card spend, online and offline. No minimum spend, no cap, credited by the 15th of the following month.

- FX fees: Real 0% at the mid-market rate across 150+ spend currencies. Hold and exchange 8 currencies in-wallet (SGD, USD, EUR, GBP, JPY, HKD, AUD, CHF).

- Annual fee: S$0/month.

- Approval: Fast onboarding via Singpass MyInfo Business in under 5 minutes, email approval within 1–2 business days. No credit check required.

- Network: Mastercard.

👉 Best for: SMEs with heavy cross-border spend such as SaaS subscriptions, digital advertising, payment platforms, and overseas suppliers. The 0% FX is structural rather than promotional, and unlike Wise or Revolut, it pairs that with 1% cashback and no monthly fee.

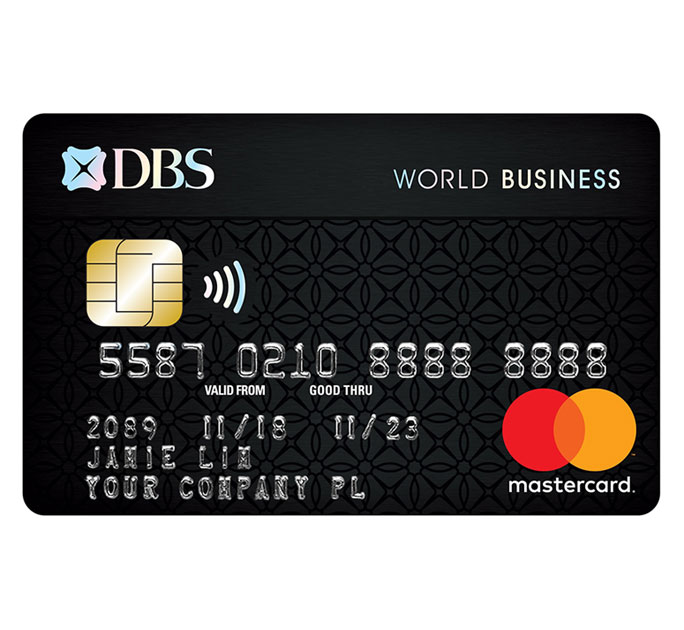

DBS World Business Card: Best Bank Card for Local Spend + Travel Perks

Image Credits: DBS

DBS’s flagship SME card with a mix of cashback rewards and travel benefits.

- Rewards: 2% cash rebate on foreign currency transactions, 1% on local dining, entertainment and travel, 0.3% on all other transactions. A promotional 8% cashback runs in the first 3 months from card issuance (min S$1,000/month spend, capped at S$240 total), but promos like this change, so check DBS’s current offer before applying.

- FX trade-off: That 2% rebate sits on top of DBS’s foreign-currency cost of roughly 3.25% all-in (a 2.25% DBS admin fee plus a 1% network conversion factor), so overseas spend still carries a net cost, just a smaller one than the full markup.

- Annual fee: S$414.20 (inclusive of GST), 1-year waiver.

- Lounge access: 10 complimentary visits per annum via Priority Pass.

- Network: Mastercard.

👉 Best for: Established SMEs with strong local spend and frequent travel who value lounge access alongside rebates.

OCBC Business Credit Card: Best for Eco-Friendly and Sustainability-Focused Spend

Image Credits: OCBC

OCBC’s SME corporate card leans into a sustainability angle on the rebate structure.

- Rewards: Up to 3% rebate at selected eco-friendly merchants, 1% on foreign currency transactions, 0.2% on SGD transactions. No minimum spend, no rebate cap.

- Annual fee: S$196.20 (inclusive of GST).

- Network: Visa or Mastercard (your choice at application).

👉 Best for: SMEs purchasing from sustainability-linked or OCBC-partner merchants. Strong niche upside, but low base SGD earn rate.

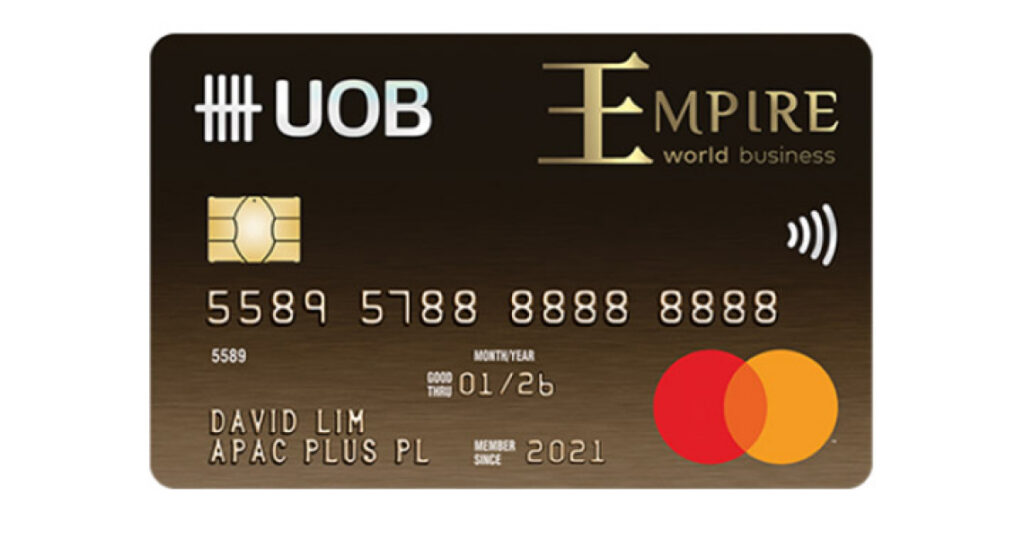

UOB Empire World Business Mastercard: Best Bank Card for Lounge Access

Image Credits: UOB Singapore

UOB’s higher-tier business Mastercard, issued by invitation. UOB was named Best SME Bank in Singapore and Asia Pacific by The Asian Banker in 2025.

- Rewards: Up to 1.5% cash rebate (1% on local spend, 1.5% on overseas spend), with a minimum S$500 qualifying spend per month.

- Lounge access: Access to over 1,300 airport lounges in 140+ countries, plus UOB Travel Concierge service.

- Annual fee: S$387.10 (inclusive of GST), first year waived.

- Network: Mastercard.

👉 Best for: SMEs already banking with UOB that receive an invitation and prioritise travel perks over pure cashback optimisation. It’s not openly applicable, so it’s only on the table if UOB extends it to you.

Maybank Business Platinum Mastercard: Best Low-Fee Travel Insurance Card

Image Credits: Maybank

Maybank’s entry-level SME corporate card with a low annual fee and broad insurance cover.

- Rewards: 1 TREATS Point per S$1 spent on eligible local and overseas spend, redeemable for airline miles (Asia Miles, KrisFlyer, Enrich) or cash credits via Pay with Points. The effective return is modest once converted, roughly 0.4 miles per S$1 or around 0.29% as cashback.

- Annual fee: S$196.20/year (inclusive of GST), waived for the first 2 years. Each supplementary card carries the same S$196.20 fee (also typically waived for the first 2 years), as business cards charge per cardmember rather than waiving supplementaries.

- Travel insurance: Complimentary cover up to S$1,000,000 (accidental death or permanent disablement) when air tickets or travel packages are charged in full, plus luggage and missed-connection cover.

- Network: Mastercard.

👉 Best for: Businesses that value travel insurance more than high cashback returns.

American Express Singapore Airlines Business Credit Card: Best for SQ Miles

Image Credits: Singapore Airlines

The only corporate card in Singapore co-branded with Singapore Airlines and built around HighFlyer points (1:1 to KrisFlyer miles).

- Earn rate: Up to 8 HighFlyer points per S$1 on eligible SQ and Scoot bookings, 2 points per S$1 on KrisShop and Pelago, 1.2 points per S$1 on all other eligible spend (no cap). 1:1 to KrisFlyer miles, up to 150,000 miles per KrisFlyer account per year.

- Annual fee: S$400 (inclusive of GST). No first-year waiver on the principal card; the first two supplementary cards are permanently waived.

- Network: American Express.

👉 Best for: SMEs with frequent Singapore Airlines travel. Limited acceptance outside major merchants means a backup card is often required.

Aspire Corporate Card: Best for SaaS & Ad Spend Startups

Image Credits: Aspire

Singapore-founded fintech corporate card, focused on startups and digital-native SMEs.

- Cashback: 1% on qualifying spend, scoped to online marketing channels (Facebook, Google, LinkedIn, TikTok) and SaaS tools (e.g. Microsoft 365, HubSpot, Slack, Notion). Other spend does not earn any cashback.

- FX: Premium plan offers 0% FX on the first S$13,000 converted per month. Card-spend FX markup outside that allowance varies by plan, so check Aspire’s current pricing.

- Card fees: Zero card activation fees and zero card transaction fees.

👉 Best for: Startups with predictable SaaS and marketing spend patterns.

WorldFirst World Card: Best Fintech Alternative for Cross-Border E-Commerce

Image Credits: WorldFirst

WorldFirst (Ant Group) is a global multi-currency account with a virtual Mastercard debit card sitting on top, so it’s a debit rather than a credit product. Strong fit for SMEs doing cross-border e-commerce.

- Cashback: Up to 1.2% monthly cashback, uncapped, on every eligible card transaction. This is a promotional rate with an end date, so check WorldFirst’s current offer.

- FX: 0% FX fees when you pay in any of 16 supported currencies.

- Annual fee: No annual card fees.

- Network: Mastercard.

👉 Best for: Cross-border e-commerce sellers with CNH (offshore yuan) exposure (1688/Alibaba sourcing, Tmall payments) where WorldFirst’s China rails are an advantage.

Wise Business: Best for Holding and Paying in Many Currencies

Image Credits: Wise

The multi-currency account most SMEs already know, with a business debit card on top. Licensed by MAS as a major payment institution.

- Card: Wise Business debit card (Visa/Mastercard), virtual instantly plus physical. First card free; extra team cards around S$4 each.

- FX: Mid-market rate plus a conversion fee from 0.26% on card spend (from 0.43% on transfers). This is not 0% FX, but the fee is transparent and among the lowest for pure currency conversion.

- Hold: 40+ currencies in one account.

- Fees: S$99 one-time account setup, then no monthly or annual fee. Free ATM withdrawals up to S$100/month, then 1.75% (and Wise cards can’t be used at Singapore ATMs).

- Approval: ACRA-registered business plus director verification; typically approved within a few days.

👉 Best for: SMEs that pay and get paid in many currencies and want the cheapest transparent conversion, without needing cashback.

Revolut Business: Best All-in-One Account with FX Allowances

Image Credits: Revolut

A business account, expense cards, and FX in one app, on monthly plans. Licensed by MAS (Revolut Technologies Singapore).

- Cards: Prepaid/debit expense cards (Visa), physical and virtual, with per-card limits and controls. First physical card per member is free; S$79.99 beyond your plan allowance.

- Plans: Basic S$0, Grow from S$15/month, Scale from S$84/month, Enterprise from S$417/month (the lower prices are on annual billing).

- FX: Interbank rate up to a monthly allowance that scales with plan (Basic S$1,500, Grow S$13,000, Scale S$60,000), then 0.6%. A 1% markup applies on weekend exchanges.

- Hold: 25+ currencies; spend in 150+.

- Approval: Fully-registered SG company (no sole proprietors); approval targeted within 24 hours.

👉 Best for: SMEs that want budgeting, multi-user cards, and bank-like tooling in one app, and whose monthly FX fits inside a plan allowance. Note there is no standing cashback on card spend in Singapore, only partner perks.

Airwallex: Best for Global E-Commerce Operations + 1% Cashback

Image Credits: Airwallex

A multi-currency business account built for cross-border operators, with a Visa debit card and unlimited 1% cashback. Licensed by MAS as a major payment institution.

- Card: Airwallex business Visa debit card, virtual and physical, up to 10 free cards on the free plan, with merchant-category and spend controls.

- Cashback: Unlimited 1% (1% on digital ads and 1% on all other local and international card spend); terms and conditions apply, so check current caps.

- FX: 0% foreign transaction fee when you spend from a matching held balance. Otherwise it auto-converts at Airwallex’s stated rate of about 0.4% above interbank for major currencies (0.6% for others).

- Fees: Explore plan free with no monthly fee; Grow S$79/month and Accelerate from S$399/month (excl GST) add more tooling.

- Approval: Incorporated SG business plus standard KYC documents; can be transacting in as little as one business day.

👉 Best for: SMEs running cross-border e-commerce or global payouts that want strong FX tooling plus 1% cashback.

Multi-Currency Business Accounts, Side by Side

If your spend is FX-heavy, these five sit in the same bracket. The differences that actually matter are how each charges FX on card spend, whether you earn cashback, and the monthly cost.

| Provider | FX on card spend | Cashback | Hold currencies | Account fee |

|---|---|---|---|---|

| YouBiz | Real 0% at the mid-market rate (150+ spend currencies) | Unlimited 1% | 8 | S$0 |

| Wise Business | Mid-market + from 0.26% (not 0%) | None | 40+ | S$0/mo (S$99 setup) |

| Revolut Business | Interbank up to plan allowance, then 0.6% (+1% weekends) | None standing (SG) | 25+ | S$0–S$84+/mo by plan |

| Airwallex | 0% from a matched balance, else ~0.4–0.6% above interbank | 1% (T&Cs apply) | 20+ | S$0 (Explore); paid tiers from S$79/mo |

| WorldFirst | 0% in 16 currencies (from held balance) | Up to 1.2% (promotional) | 20+ (incl. CNH) | S$0 |

All five are licensed by the Monetary Authority of Singapore (MAS) as payment institutions. FX, fees and cashback are accurate at time of writing; verify on each provider’s site before applying.

TL;DR:

- YouBiz is the only one of the five that pairs genuine 0% mid-market FX with a standing 1% cashback and no monthly fee.

- Wise wins on the sheer number of currencies you can hold and on transparent transfer pricing

- Revolut bundles the most account tooling but charges FX once you exceed a plan allowance

- Airwallex is strongest for high-volume cross-border operators

- WorldFirst is the pick for China-sourcing e-commerce.

The Best Corporate Card Depends on Your Priorities

There is no single “best” corporate card for every SME. The right choice depends on what your business is optimising for.

If you’re a startup

Early-stage businesses often face stricter requirements from traditional banks, including operating history, financial statements, and sometimes personal guarantees. Fintech options such as YouBiz and Aspire typically take a different approach, relying on ACRA registration and Singpass verification instead of credit history. The trade-off is that these solutions are usually prepaid or wallet-based, meaning there is no credit float, something most cashflow-managed startups can comfortably work around.

If your goal is miles

The American Express Singapore Airlines Business Credit Card is the most direct route for earning KrisFlyer miles from business spend, especially on Singapore Airlines and Scoot bookings. However, for general overseas or operational spend, FX fees can significantly reduce the effective value of those miles, especially if spend is not concentrated on travel.

If you bank primarily with one provider

Many SMEs naturally gravitate toward the corporate card linked to their operating bank for convenience and integration. Established banks such as DBS and UOB offer bundled ecosystems that can simplify approvals, expense tracking, and account management if your business already banks with them.

If most of your spend is overseas

For businesses with high foreign-currency spend, FX costs often matter more than headline cashback rates. Even modest rebates can be outweighed by FX markups over time, which is why multi-currency accounts (YouBiz, Wise, Revolut, Airwallex, WorldFirst) are often considered in this segment.

Don’t Overlook FX Fees: They Quietly Eat Your Rewards

One of the most common mistakes SMEs make when choosing a corporate card is focusing on cashback rates while overlooking foreign exchange fees.

Most corporate cards in Singapore charge between 2.5% and 3.5% on foreign-currency transactions. While a card may advertise 1%–2% cashback, the FX markup can often exceed the value of the rewards earned, resulting in a net cost on overseas spending.

Example: a typical SME spend profile

Assume a business spends:

- S$60,000 per year on overseas suppliers, SaaS subscriptions, and foreign-currency expenses

- S$30,000 per year on local SGD expenses such as office supplies, dining, and operational costs

Scenario 1: Traditional corporate card (FX fee 2.5%, 1% blended cashback)

| Item | Amount |

|---|---|

| FX costs on overseas spend | S$1,500 |

| Cashback earned | S$900 |

| Net impact | −S$600 |

Scenario 2: YouBiz (0% FX, 1% cashback on eligible spend)

| Item | Amount |

|---|---|

| FX costs on overseas spend | S$0 |

| Cashback earned | S$900 |

| Net impact | +S$900 |

In this simplified example, the difference between the two setups is S$1,500 per year, before accounting for any annual card fees.

Why FX often matters more than rewards

For businesses with meaningful overseas spend, reducing FX costs can have a larger financial impact than increasing cashback rates.

This is particularly relevant for companies that regularly pay:

- Overseas suppliers

- Software subscriptions

- Cloud infrastructure providers

- Digital advertising platforms

- International freelancers and contractors

On the other hand, businesses whose spending is largely local may benefit more from cards that offer enhanced rebates on dining, travel, or other specific categories.

Before comparing cashback rates, understand how much your business spends in foreign currencies. In many cases, that’s the number that has the biggest impact on your overall cost.

Final Takeaway

There is no single corporate card that is best for every SME.

Businesses with heavy local dining, travel, or airline spend may get more value from specialised bank cards or miles programmes. Businesses that prioritise lounge access, travel insurance, or banking integration may also prefer a traditional issuer.

However, for SMEs with significant overseas spend (whether that’s software subscriptions, digital advertising, supplier payments, or cloud infrastructure), the economics often look different. In these cases, reducing FX costs can have a greater impact than chasing higher reward rates.

That’s why many SMEs evaluating their business spending stack are increasingly considering multi-currency solutions such as YouBiz. Rather than offsetting FX fees with rewards, YouBiz focuses on eliminating FX costs altogether while still providing cashback on eligible spend.

FAQ

There isn’t a single answer for every business. The best option depends on your spending profile, business stage, and whether you prioritise cashback, miles, travel perks, or low FX costs.

For SMEs with significant overseas spend, a multi-currency business account like YouBiz can complement or even replace a traditional corporate card.

Businesses with heavier local dining, entertainment, or travel spend may find additional value in bank-issued corporate cards from DBS, OCBC, UOB, or Maybank.

All four are MAS-licensed multi-currency accounts, so the differences come down to FX, cashback, and cost.

– YouBiz applies a genuine 0% mid-market FX rate and pays unlimited 1% cashback with no monthly fee.

– Wise charges a transparent conversion fee from 0.26% on card spend and offers no cashback.

– Revolut gives an interbank FX allowance that scales with a paid monthly plan, then charges beyond it, and has no standing card cashback in Singapore.

– Airwallex offers 1% cashback and 0% FX when you spend from a matching held balance.

The right pick depends on whether you value cashback, the number of currencies you hold, or the breadth of account tooling.

Accepting payments is separate from business spending. Popular options in Singapore include Stripe, DBS MAX, NETS QR, and PayNow QR. Stripe and DBS MAX support card acceptance for SGD and major foreign currencies, while PayNow QR remains one of the most widely used methods for local transfers.

YouBiz also provides businesses with a PayNow QR code for receiving SGD payments without additional setup fees.

Most providers require an ACRA-registered Singapore business, such as a private limited company, sole proprietorship, partnership, or LLP. Requirements vary by issuer.

Traditional bank cards may require additional documentation, while fintech providers such as YouBiz, Aspire, Wise, and Airwallex generally offer a more streamlined onboarding process. Some, like Revolut Business, do not onboard sole proprietors, so check eligibility before applying.

Approval timelines vary across providers. Traditional bank-issued corporate cards can take several weeks depending on the application and verification process.

YouBiz applications are completed through Singpass MyInfo Business, with approval typically issued within 1–2 business days. Once approved, the virtual Mastercard is available immediately in the app, while the physical card typically arrives within 5–7 working days.

No. A prepaid business card is funded from your available account balance and does not provide a credit line. A corporate credit card provides a credit facility that is repaid later according to the card issuer’s billing cycle.

Businesses that prioritise spend control and lower barriers to entry often prefer prepaid solutions, while businesses that require short-term working capital may prefer a traditional credit card.

Built for the Way Modern SMEs Spend

Software subscriptions, cloud infrastructure, digital advertising, payment processing fees, and overseas suppliers now make up a growing share of business expenses. YouBiz was built with these spending patterns in mind.

With 0% FX fees across 150+ currencies, unlimited 1% cashback on eligible spend, no monthly fees, and fast onboarding through Singpass MyInfo Business, it helps SMEs spend globally without the hidden costs often associated with traditional corporate cards.

Apply in under 5 minutes at you.co/biz. Once approved, your virtual Mastercard is available immediately, while your physical card arrives within 5–7 working days.

Already saving on overseas spend? Refer another business owner and you each earn S$50 when they sign up and make their first card spend.